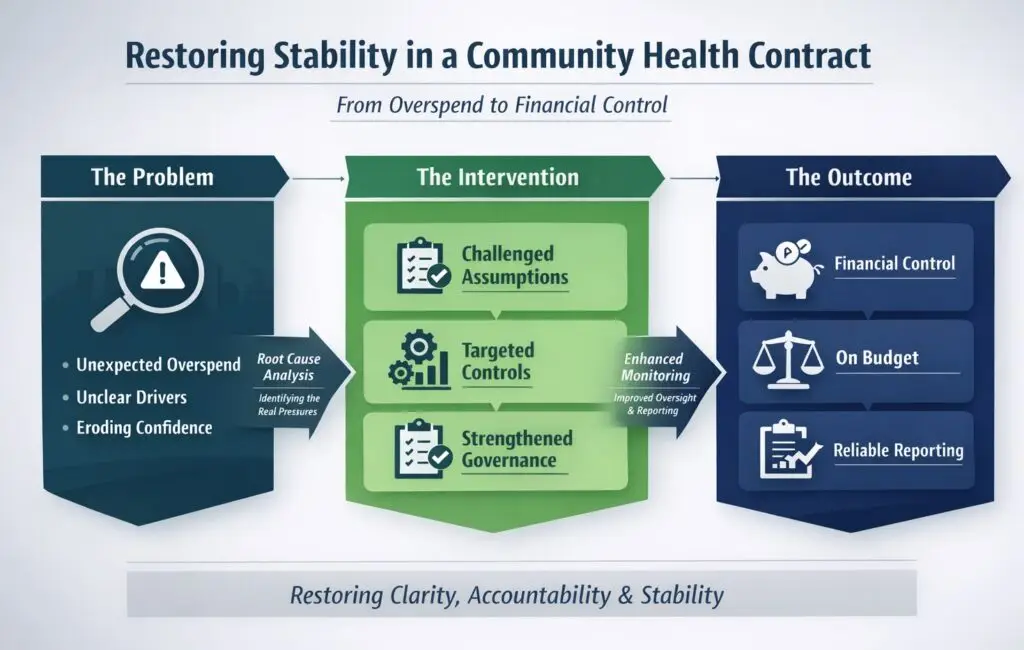

When a new community health contract goes live, there is always a period of bedding in, during which systems are refined, demand patterns settle and operational practice aligns with contractual expectations. In this case, however, what initially appeared to be normal early stage variation gradually developed into something more serious: a significant and unexpected overspend that began to threaten both the affordability of the model and confidence in the long-term sustainability of the service.

The financial variance was material, it was accelerating and, most concerningly, it was not clearly understood.

Senior leaders understandably required assurance that the service remained viable and controllable, commissioners needed clarity on whether the model itself was flawed and the provider, although cooperative, was unable to articulate with precision what was driving the increased expenditure. Reports described the position, but they did not explain it. Forecasts changed month to month, workforce costs appeared disproportionate to planned activity and assumptions were presented without sufficient evidence to support them.

The risk at that point was not merely financial; it was reputational, relational and strategic. Without intervention, confidence in the contract architecture itself could have eroded.

Re-Establishing Clarity Through Structured Analysis

Rather than responding reactively by imposing blunt financial restrictions, we made a conscious decision to slow the process down and introduce structure, bringing together commissioners, finance colleagues and both operational and financial leads from the provider into a single, focused forum with a clear purpose: to undertake a disciplined root-cause analysis that would separate genuine cost pressures from modelling error, operational drift or precautionary over-resourcing.

The discussion was reframed around three interconnected lenses. First, we examined activity drivers in detail, exploring whether demand had genuinely exceeded forecast, whether referral pathways had shifted in practice or whether interpretation of eligibility criteria had expanded beyond the original contractual assumptions. Secondly, we scrutinised the workforce model, mapping staffing levels directly against verified activity data in order to test whether resource growth was proportionate or precautionary. Thirdly, we reviewed the forecasting methodology itself, challenging whether projections were grounded in evidence or constructed around worst-case scenarios that had gradually become embedded as assumed reality.

This approach changed the tone of the conversation. What had previously been a defensive exchange became a collaborative exercise in evidence gathering, because the focus moved from attribution of fault to restoration of clarity.

Challenging Assumptions and Resetting Expectations

As the analysis progressed, several assumptions that had initially been presented as fact did not withstand detailed scrutiny. Apparent demand growth, once disaggregated, reflected short-term fluctuation rather than sustained trend; certain staffing increases had been introduced as precautionary capacity rather than as a response to confirmed workload; and forecast trajectories had been modelled on upper-range scenarios without clear probability weighting.

At this stage, it was important to be both firm and measured. We challenged the evidence base underpinning these positions, not in an adversarial manner but with the clear expectation that public funds require transparent justification. We reset reporting standards so that every material cost line had to be explicitly linked to verified activity, and every forecast assumption had to be traceable and defensible.

In effect, we restored commercial discipline without destabilising the provider relationship, reinforcing that accountability and partnership are not mutually exclusive.

Implementing Targeted Corrective Controls

Once the genuine drivers had been isolated and the speculative elements stripped away, we agreed a corrective plan that was proportionate rather than punitive, recognising that sustainable recovery requires precision rather than reaction.

Workforce controls were introduced through tighter vacancy management, clear establishment ceilings and alignment of any temporary staffing to evidenced demand rather than anticipated growth. Activity monitoring was strengthened so that referral patterns and eligibility interpretation were reviewed consistently, allowing early identification of variance before it translated into financial drift. Forecasting processes were standardised, introducing structured templates, monthly reconciliation of assumptions and scenario modelling that distinguished between probable and possible outcomes.

The objective was never to diminish service quality, but to ensure that the relationship between demand, resource and expenditure was transparent and predictable.

Strengthening Governance and Restoring Assurance

Financial instability often signals not operational failure, but insufficient governance intensity. Accordingly, oversight mechanisms were strengthened through fortnightly integrated performance and finance meetings, clearer escalation routes for emerging risks and improved synthesis of financial data with quality metrics so that cost control did not occur in isolation from service standards.

We ensured that senior leadership received regular, structured briefings that articulated not only the scale of the risk, but also the corrective trajectory and confidence levels in forecast recovery. Visibility created assurance, and assurance rebuilt confidence.

The Result

Within two quarters, variance had reduced to within acceptable tolerance, forecast accuracy had materially improved and financial control was demonstrably re-established. By the beginning of the second contractual year, the service was operating within budget, reporting had stabilised and governance arrangements had become embedded rather than reactive.

What had initially presented as a destabilising financial threat ultimately became an example of how disciplined contract management, structured challenge and strengthened oversight can restore stability without compromising delivery.

The Broader Lesson

Overspend rarely emerges overnight; it develops gradually in the space between assumption and evidence, between precaution and necessity and between reporting and true understanding. The turning point in this case was not a single financial adjustment, but the reintroduction of analytical rigour and clear accountability.

When commercial oversight restores line of sight from activity to cost and from forecast to evidence, stability follows.